The past few years have been pretty wild. But don’t take my word for it. Don’t even take your memory for it. Here’s the data:

A once-in-a-century pandemic ravaged the world. We’ve now seen over 636 million people with a confirmed case of COVID-19. And probably billions more that never knew or reported it:

In an attempt to keep the wheels from flying off our economy during this time, the FED lowered interest rates to the floor, then threw the car into reverse and slammed on the gas in 2022:

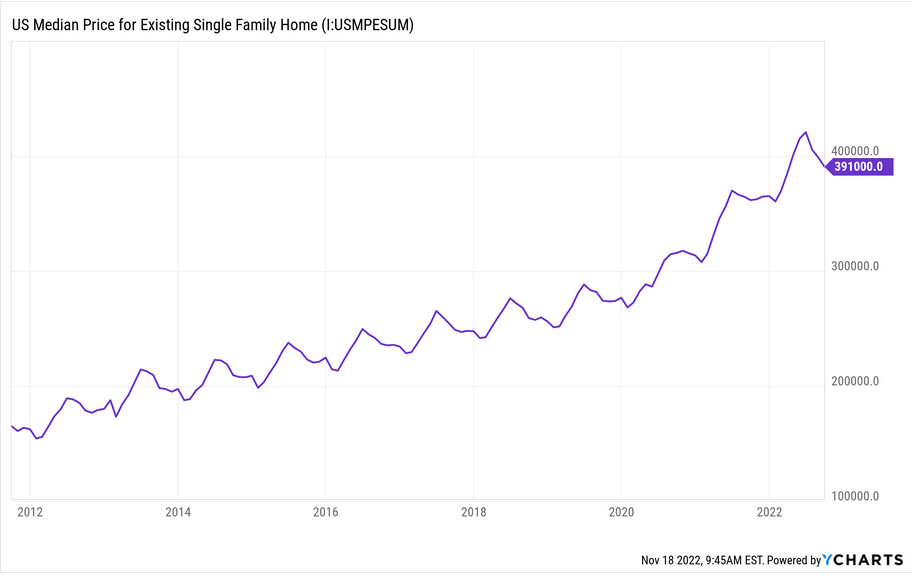

Interest rates at near-zero and the government spending billions on mortgage-backed securities induced a housing boom which was then fueled by stimulus checks and a desire for more space to work from home. Here’s the median house price in the U.S.:

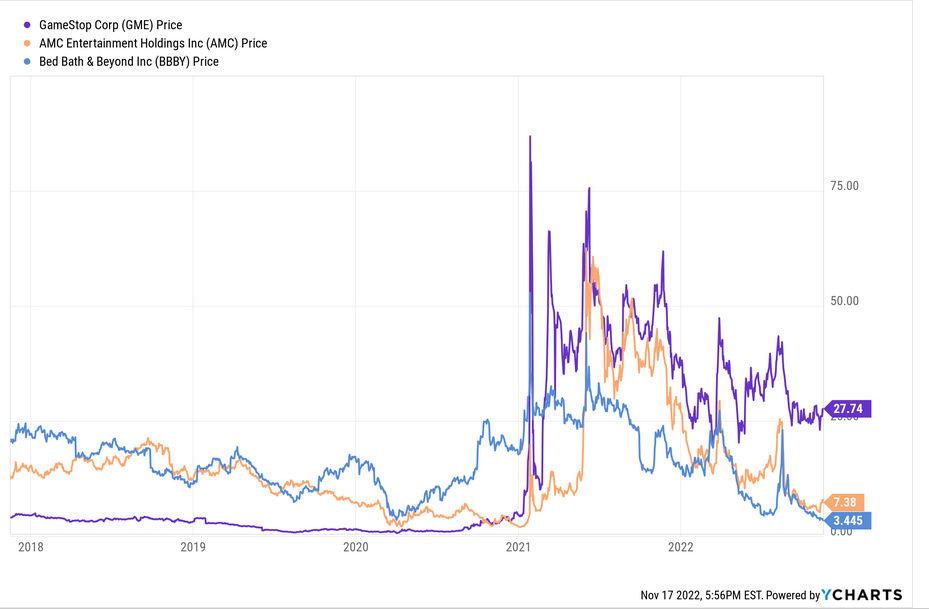

Armed with those stimmy checks and boredom, everyone “quiet quit” their jobs to become day traders in meme stocks in an attempt to cause a short squeeze (spoiler alert, the hedge funds won):

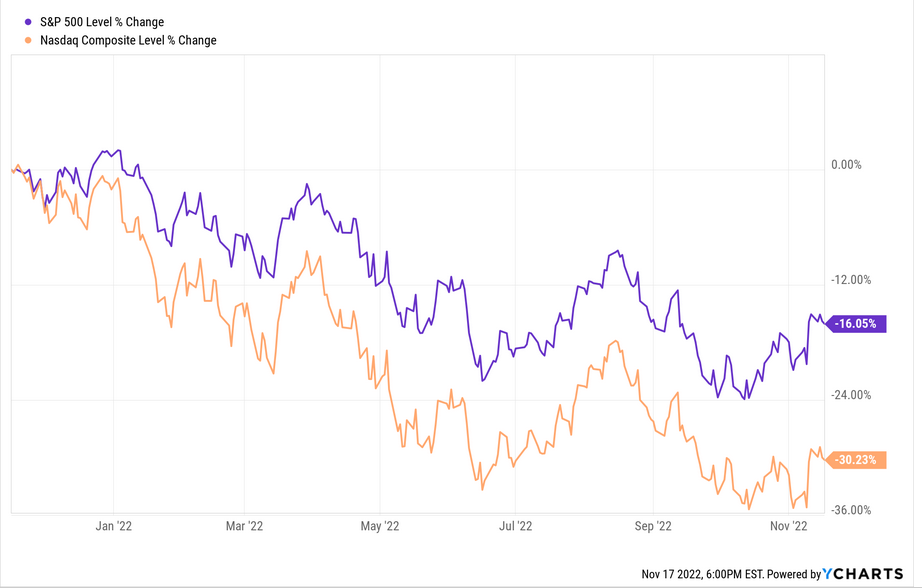

If you thought 2020 and 2021 were weird years for the market (and the world), you were right. But the stock market is one big mean-reverting machine as I explained in my open letter to no one. What goes up must come down. Here’s how far the major indices have fallen from their all-time highs:

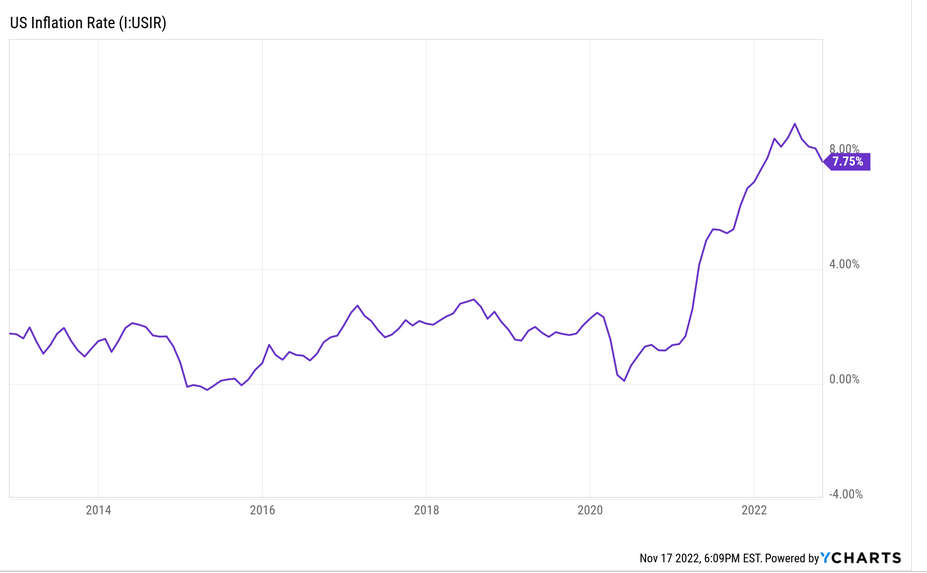

But this bear market did not come out of nowhere. It’s largely been caused by a massive uptick in inflation and the government’s response to contain it (which has been to raise rates in an attempt to lower wages via job cuts, cause a recession, and generally drive around using the rear view mirror):

And just for good measure, let’s not forget crypto’s unfortunate place in all this. Here’s the percent drop from the highs of several notable coins (unsurprisingly, the FTX blow up has not helped):

These charts are giving me whiplash.

Let’s pivot like everyone hopes the FED will and talk about how I’m managing my own money throughout all of this and hopefully you get some ideas on how to manage your own.

With interest rates at 4%, the new risk free rate is, you guessed it, 4%. That’s because you can now buy 2-Year U.S. Treasuries and earn 4.46%. This means the opportunity cost to own equities has gone way up. It also means cash now has a yield again.

Most online savings accounts and some brick and mortars are giving 3% interest rates on cash. There’s your start. I am personally holding a lot more than normal because 1. it feels good to earn 3% even if that means I’m actually losing 4% due to inflation and 2. I want to finish my basement. But if the market crashes another 20%, I’ll hold off on finishing my basement and use the cash there instead.

In the meantime, with inflation as high as it is, Series I Bonds are still earning double savings account yields. So I bought two Series I Bonds each at the annual limit (one for me and one for my wife) which will earn 9.62% for the next 6 months and will then earn 6.89% for the 6 months after that. At which point, I can redeem them both or let them continue to grow if inflation stays high. (Fun fact: the “I” stands for inflation.)

Because I’m holding more cash than normal, I’ve also increased my taxable account monthly contributions into VTI. Dollar cost averaging into down markets is one of the single best predictors of strong forward returns. Here are my purchases throughout 2022:

It feels a little nerve-wracking investing in this market but I’m playing the long game here. I’m not buying individual stocks (I don’t have the stomach for it anymore) and I’m doing it on a set schedule to take emotion out of the equation.

Unless you are about to retire, you should be cheering for market drops like this. It is a momentary chance to shop brand names at marked-down prices. Buy them via index fund to eliminate most of the risk.

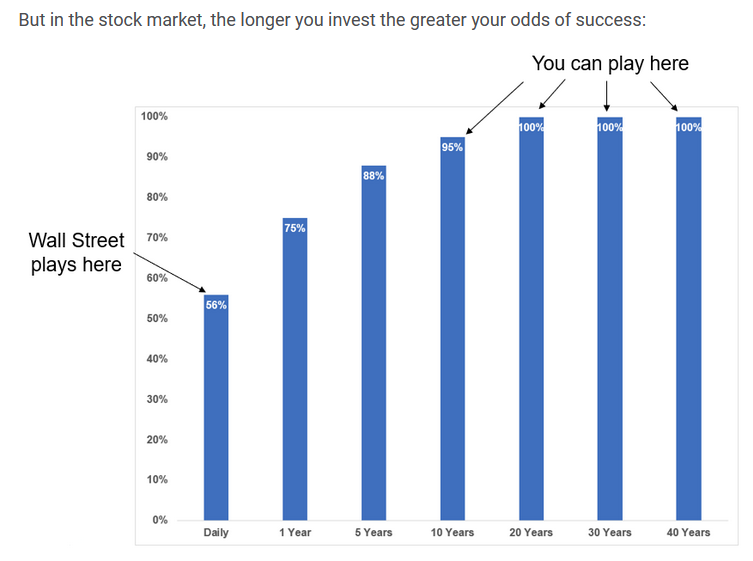

Ben Carlson has a great point about the longer you stay invested, the better your odds are of a positive return over various lengths of time:

Because a few of my early 2022 stock purchases had taken such a massive hit, I decided to sell them to take advantage of tax loss harvesting for some other capital gains I wanted to realize this year. If you own any individual stocks and want to tax loss harvest them, you need to sell them before Dec. 31 for the current year.

Finally, I’ve been maxing out my Roth IRA and Roth 401(k). If you haven’t been, now is a great time to increase your contributions and try to squeeze a bit more juice out of this bear market.

It’s also a good time to come up with a game plan for maxing out 2023 retirement accounts which will have increased limits. Need tips on saving money? More here. And here.

Until next time, internet friends.

More reading:

What Is a Buyer-Agent Agreement – And Why It’s the Smartest Move You Can Make When Buying a Home

Buying a home is too big of a decision to go it alone or leave it to chance. That’s where a Buyer-Agent Agreement comes in.

Keeping Up with Yourself

Keeping up with yourself can be a great fuel—and an even greater trap. The art is knowing when to press forward, and when to simply be where you are.

(5 min read)

Why You (and I) Need a Career Coach

I messed up at work but survived — thanks to my career coach. Spoiler alert: British football analogies included.

You must be logged in to post a comment.