A housing market that outpaces wage growth at every possible turn. A pandemic that continues to stutter the global economy and cripple Fortune 500 companies. Enough social unrest to spark a new civil war. The world travel industry crushed under the weight of itself. Stock prices more volatile than Michigan weather. All topped with a U.S. election that will only fuel this dumpster fire of a year.

So Where the Hell Should I Invest My Money During a Year Like 2020?

I really have no idea.

This game is anybody’s guess. But I will tell you where I am putting it and why.

The following timeline shows the general changes I’ve made to my portfolio over the last year, when I made the change, and why.

January 2020

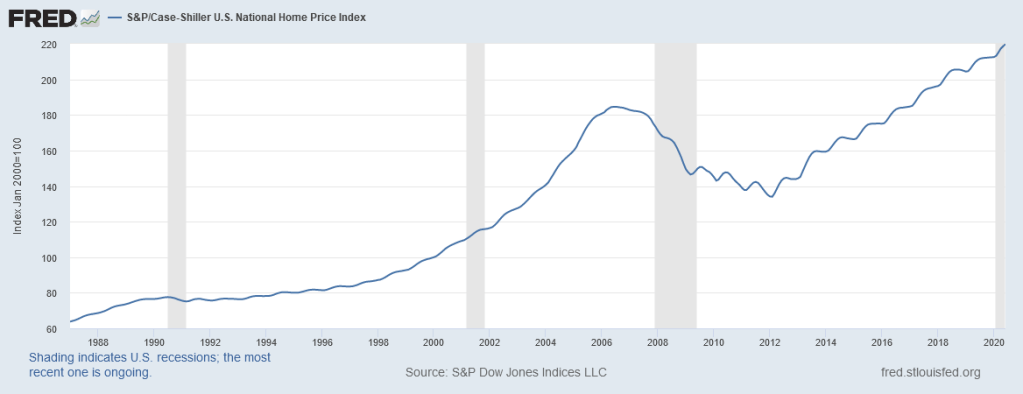

In late 2019, with house prices sharply improved, as measured by the Case-Shiller index, and the stock market racking up gains like Schwarzenegger in the 70s, I decided to sell my biggest asset (my house) and hold the cash for any potential buying opportunities. I didn’t know when or why it would happen, but I was betting on a decline of some sort.

Case-Shiller housing index:

S&P 500 YTD Performance for 2018, 2019, and 2020:

Lest I pat myself on the back, this sort of outcomes-based analysis can be really toxic and I definitely made some mistakes with my timing. For example, I spoke with my real estate agent recently and he told me I could have made about 15% more on my house if I had waited until this year to sell (simple supply and demand). But having purchased the house in 2013, I was happy enough with my return on the investment at the time.

I recognize that not many people can sell their homes and downsize into an apartment. Being unmarried with no kids and very few possessions by design, it was doable for me.

So that’s the first step I made going into 2020 – pull out of my real estate position almost entirely. Keep reading below for how I continue to invest in real estate while not owning a home.

February 2020

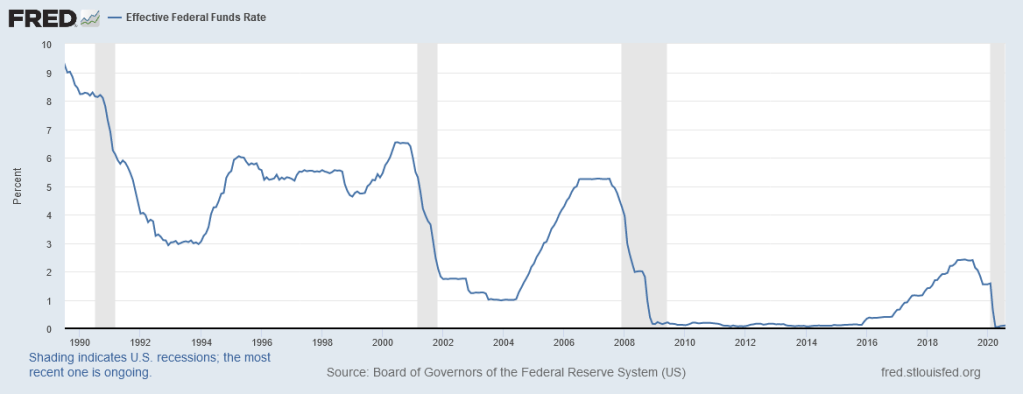

In early February, with interest rates still very attractive and no real concern of COVID-19 in the States, my online savings account was paying yields of almost 2% on general savings, and about 2.5% on Certificates of Deposit. My cash was simply sitting on the side lines in the online savings account during this time.

I also made my 2019 Roth IRA contributions and dedicated half to gold and half to a target-date 2055 fund.

Warren Buffett is also apparently very bullish on gold in 2020. This is a storehouse kept for safety.

March 2020

As the pandemic washed ashore in the U.S. in late February and early March, we saw the fastest market selloff in history. The stock market dropped 30% in 22 days. For context, the next three fastest selloffs occurred during the Great Depression and have been studied for decades as one of the worst financial periods in modern history. Not a good sign that we beat those three to first place.

In late March, I got to work buying some stocks that had been beaten up pretty badly as more and more news was coming out about the pandemic. I bought stocks mainly in the travel, oil, and automotive industries. A few cyclical and tech stocks sprinkled in, too, but we had no idea how much this would disrupt our analog lives yet. I did not purchase as many tech stocks as I should have.

April 2020

Over the course of March and April, I invested about 30% of my cash savings in stocks, not including my safety net of living expenses. I was and still am weary of where the “bottom” to the COVID market might be. Some people forget that it wasn’t until March 2009 that the financial crisis hit rock bottom. This was many months after the initial decline of stocks in early 2008 and many people thought we were out of the woods.

Cash on hand is not the best idea with the FED pumping as much liquidity into markets as they are right now, and keeping interest rates at 0% for the foreseeable future, because inflation is going to be an issue. But if you are unsure of the fallout of a pandemic, the likes of which have not been seen in a hundred years, the safe bet is to play both sides.

April was also the month I increased my 401(k) contributions, even though my company cancelled their matching program. My 401(k) is a good way for me to eliminate the “itch” to check my investments each day because I know I won’t touch that money for many years to come. It takes the psychological factor out of investing for me. Bad news headlines are irrelevant on a long enough timeline.

May 2020

In May, unsure of how long the virus was going to last and worried about being too heavily invested in stocks only, I took from my cash savings and doubled my real estate investment. I don’t own a house or any rental properties but I do have access to a REIT (Real Estate Investment Trust) and so do you.

I personally have an account with Fundrise, but there are competitors you can find. Fundrise is an investment firm focused solely on real estate developments like shopping centers and apartment buildings.

They manage over 4.7 billion dollars of assets from a group of 130,000+ investors. It’s really cool to see the precise projects I am invested in, some of which are right in my own city. I can literally drive past the construction site of my investment and see the progress.

June 2020

In June, as I watched the rebound of stocks grow and grow, I decided it was time to contribute up to the 2020 limit in my Roth IRA. I put it entirely towards a total U.S. Stock Market Index Fund with a low expense ratio.

Check out my article here about choosing stocks and mutual funds:

Evaluating Stocks: 33 Questions I Use to Research and Select a Stock or Mutual Fund

Use these common sense questions to pick your next stock or mutual fund. (6 min read)

July 2020

In July, I added about 10% more of my cash savings into tech and some smaller biotech companies that I have my eye on. I also invested in a few China-based companies to give me some more exposure to that huge recovering market. At this point, about 40% of my original cash savings have been allocated to individual stocks.

August 2020

In August, after seeing the euphoria in the tech sector of the stock market, I became weary of tech stocks in general and actually sold my position in Tesla right after they announced their stock split. I missed out on another 60% gain as Tesla continued to skyrocket, but I am happy with my decision.

Stocks are bought for the long haul. I didn’t sell any others. I just wanted to be contrarian and I think Tesla was too overpriced.

The S&P 500 has just about made up all the ground it lost to the pandemic in March, but where it goes from here is impossible to predict. Anyone telling you they know what will happen over the next 12 months is lying or trying to sell you something, or both.

September 2020

A few days into September, and the NASDAQ has had a few sharp declines on back to back to back days. This is to be expected with such a meteoric rise. If prices become attractive enough, I will allocate another 5-10% of my cash to the tech sector specifically.

We need selloffs like this to counter-balance the “dumb” money from the masses. (Spoiler alert, retail investors like us are the “dumb” money, but retail investors only make up about 20% of all investments, so if we’re dumb, so are the suits because just 20% doesn’t move the needle from zero to sixty like we’ve seen.)

Travel stocks should do well when a vaccine is widely available, so I am also keeping my eyes on those. Once vaccine efficacy is proven, money will likely flow out of tech and into airlines, hotels, and entertainment stocks. That might not be for awhile, though. We still need to see what winter (and flu season) holds in store for us.

Average checking account balances are at an all-time high and travel is at an all-time low so you better believe people will be spending money on vacations over the next few years.

As for the future, you could make an argument in either direction. One of the best finance writers I read, Ben Carlson from A Wealth of Common Sense, wrote this post making both a bull and bear market case for different asset classes. Highly worth a read.

Conclusion:

Nothing written here is financial advice, it is simply my opinion and my views and is probably all wrong. But I hope that by sharing my actions during this difficult period it prompts you to consider your own investments on a micro and macro scale.

Sign up for my newsletter here:

More reading:

What Is a Buyer-Agent Agreement – And Why It’s the Smartest Move You Can Make When Buying a Home

Buying a home is too big of a decision to go it alone or leave it to chance. That’s where a Buyer-Agent Agreement comes in.

Keeping Up with Yourself

Keeping up with yourself can be a great fuel—and an even greater trap. The art is knowing when to press forward, and when to simply be where you are.

(5 min read)

Why You (and I) Need a Career Coach

I messed up at work but survived — thanks to my career coach. Spoiler alert: British football analogies included.

Something went wrong. Please refresh the page and/or try again.

You must be logged in to post a comment.