First off, well done for clicking on whatever link brought you to this article. You have officially reached the “boring adult” level in the game of life. What better way is there to spend your time than looking up the top 5 ways to improve your credit score? I literally can’t think of a single thing.

If you already understand credit and the importance of it, go ahead and skip down to the top 5 list. For the rest of us…

“What is a credit score?”

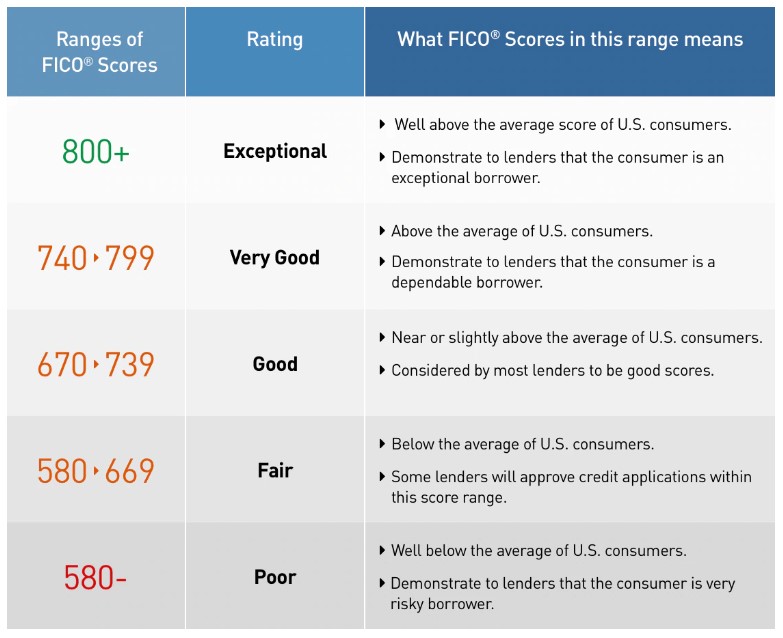

A credit score is simply a number that tells people how creditworthy you are. In other words, how likely you are to pay back a loan on time. Your specific number is calculated based on a mix of factors and ranges from 300 (the worst) all the way up to 850 (the best). The factors include things like how much debt you have, how many credit accounts you have open, and how old your accounts are.

“How can I check my credit score?”

The above website is the simplest one to use and is managed by Experian, one of the leading providers of online credit reports and scores. There is no credit card needed to check your score, and checking your score with this website will not hurt your credit score in any way. I filled out the online form and had my score in less than 5 minutes. You can also download your credit report to confirm everything looks accurate.

“Why is my credit score important?”

Well, aside from being able to brag to all your friends about how sick your credit score is, there are a few lesser important reasons that your credit score is important:

- A good credit score will make it easier for you to get approved for loans such as a car loan or a mortgage. (You are seen as more likely to pay back your loan.)

- A good credit score will let you borrow money at a lower interest rate. (The difference between a 1% interest rate loan and a 2% interest rate loan for a new car could save you thousands of dollars over the lifetime of the loan.)

- A good credit score may get you a better deal when you sign a new apartment lease. (For example, because I have a high enough credit score, my landlord waived my security deposit entirely when I moved into my new apartment.)

- A good credit score may get you cheaper car insurance. (You are seen as less risky and car insurance companies HATE risk.)

- A good credit score will make sure you can get approved for the best credit cards on the market. (Generally, these are the high “cash-back” reward credit cards which saves you money on the things you have to buy anyways.)

“Why should I check my credit score?”

You should check your credit score periodically to ensure you are improving it (or at least that it isn’t trending downwards). Monitoring your credit score (and reviewing your credit report) can help you catch things like missed payments or potentially fraudulent accounts that were opened in your name.

Checking your credit score also gives you the upper hand during negotiations for big ticket purchases. Another reason to check your credit score is to be confident you will qualify for lower car insurance premiums or high reward credit cards described above. Once you know your score has improved, simply call your insurance provider and ask them to run your score to ensure you are getting the cheapest rate possible.

This is called a “soft hit” on your credit and will not affect your score. But be careful, because if they check your score and it turns out to be lower than you thought, it may actually increase your insurance. But you’re reading this article, so chances are good you’ve done your homework.

“What’s the difference between a hard hit and a soft hit on my credit?”

A hard hit will negatively impact your credit for a short amount of time (usually a year). Sometimes hard hits are unavoidable such as when you are looking to take out a loan and are shopping around at a few different loan providers to find the best interest rate.

It is important to note that there is a 45 day grace period where the credit agencies will consider multiple hard hits as one because it is clear you are shopping around for a good interest rate. Be sure to do your shopping around all at the same time to take advantage of this fact. This does not apply to credit cards.

A soft hit is simply informational and will not affect your credit score. For example, your insurance company will run a soft hit on your credit to determine any discounts or premiums they may give you.

“How can I improve my credit score?”

Ahhh, the rules of engagement. Where the rubber meets the road. To the victor goes the spoils! And other such lofty epigrams that completely overstate how valiant it is to improve your credit score.

Without further ado…

5 Simple Ways to Improve Your Credit Score

5. Limit “hard hits” on your credit.

This is 10% of your credit score.

Someone getting multiple credit cards and loans all at once is seen as risky to lenders. They want to be sure you are not taking on too much debt all at once. Credit-seeking activities generate hard hits and is seen as risky if you have a lot of them in a short amount of time.

If you are planning to buy a car or house in the near future, it would be best not to open up a new credit card in the two years leading up to it.

4. Use different types of credits.

This is 10% of your credit score.

Showing that you are capable of managing various types of credit is a good thing to lenders. For example, you might have two credit cards (credit cards are revolving credit) and a car payment (also called installment credit).

However, never take out a loan simply to diversify your lines of credit.

3. Increase the length of time you’ve had your accounts open.

This is 15% of your credit score.

The longer the better. This is because you are seen as more experienced if you’ve had various lines of credit open for a decent amount of time. If you are young, this is simply going to hurt your score until you’ve had time to establish yourself in the world of consumer credit.

Aside from ensuring you open up at least one credit card when you are young (and use it responsibly), there’s not much you can do to improve this other than wait. Be sure to not close any credit cards unless you absolutely need to due to over-spending or something like that.

If you are over-spending, I recommend you read my article on how to spend money more in line with your values. Chances are good your money isn’t being used to increase your happiness if you are constantly maxing out your credit cards:

How Values-Based Spending Can Make You Rich

Why focusing on your values is a good place to start your path to financial independence. (8 min read)

2. Pay down your debt.

This is 30% of your credit score.

Technically, the credit bureaus that keep your score do so by using a metric called “credit utilization”. Basically, they look at how much credit (or debt) you could use vs. how much credit you actually use.

It is mainly a snapshot in time. So if you historically use most of your available credit, it will not negatively affect your score unless you are currently using most of your available credit at the time your score is pulled.

A simple example would be if you have one credit card with a limit of $1,000, and you keep a balance of $500 on average, your credit utilization rate would be 50%. Experts (including the credit bureaus themselves, say you should keep this number below 30%. However, it is important to note that people with the highest credit scores generally only use 7% or less of their available credit at any given time.

This is why it can actually be a good thing to have a few different lines of credit open. You may also consider having your existing credit card limits increased. To do so, simply call your credit card company and tell them you’d like to increase your credit limit. They will typically do a “hard hit” on your credit, and if everything looks good, they may increase your limit.

1. Pay your bills on time.

Paying your bills on time is the single most important contributor to your credit score.

This is 35% of your credit score.

Whether or not you pay back your debt on time is a great indicator of whether or not you will pay back your debt on time. Set up auto-pay whenever possible. Keep a small spreadsheet of your bills and when they are due. Keep track of your due dates and do everything you can to never miss a payment.

If you’ve missed a payment in the past, there’s no much you can do about it other than wait. Bad marks on your credit report for missed payments will fall away after 7 years.

Super Secret Credit Tip

If you made it this far in the article, you must REALLY care about your credit. Nice job! You are in good company. As a reward, here is a super secret tip that most people get completely wrong:

You do not need to carry any balance on your credit card to improve your credit score.

The reason is because the interest that you pay on a credit card is not reported to the credit bureaus. It’s not part of the algorithm to determine your credit score. Don’t believe me? Go check your credit report. There are only two numbers reported to the credit bureaus that manage your score, statement balance and available credit.

No need to pay the high interest rate when the credit bureaus don’t care about it. Pay your bills on time, and in full, every time.

If you found this article useful, please pass it on and consider subscribing to be notified of new posts:

More reading:

What Is a Buyer-Agent Agreement – And Why It’s the Smartest Move You Can Make When Buying a Home

Buying a home is too big of a decision to go it alone or leave it to chance. That’s where a Buyer-Agent Agreement comes in.

Keeping Up with Yourself

Keeping up with yourself can be a great fuel—and an even greater trap. The art is knowing when to press forward, and when to simply be where you are.

(5 min read)

Why You (and I) Need a Career Coach

I messed up at work but survived — thanks to my career coach. Spoiler alert: British football analogies included.

You must be logged in to post a comment.