Investing in real estate is a lot like giving someone a bunch of money in exchange for some wood, concrete, and glass arranged in a way that protects you from wind, rain, and inflation.

“Wow, real creative, Kevin.”

Hey, be nice! This website is free!

Now that I’m done insulting and then arguing with myself, let me explain why you might want to invest in real estate beyond the conventional wisdom.

Unlike owning stocks, cash, or retirement accounts, real estate is real place you can touch and feel. You live there. You raise kids there. You spill coffee there. It’s home.

You can’t spill coffee on your NFT.

Putting a price tag on “home” is actually quite difficult because emotions and sentimentality play a far bigger role in a home than many other investments in your life.

Houses, apartment buildings, offices, and malls aren’t correlated with stock markets and currencies. Owning real estate in any of these categories provides diversification to your portfolio. Owning real estate in ALL of those categories is even better and completely possible for anyone with as little as $10 as you will see.

In addition to diversifying your real risk, real estate helps with perceived risk. There aren’t red and green ticker symbols for every home address going up and down every week day from 9:30 in the morning until 4pm in the afternoon (or 24/7 for crypto). This makes it easier to ignore daily fluctuations in price and headlines that mighty scare you into selling.

Real estate is obviously illiquid. You cannot simply convert your house into cash like you can with your, well, cash. This is a pro and a con. It is a pro for those prone to over-spending on products or vacations each year because…

Owning real estate is also a form of forced savings. Having a mortgage on your primary residence or an apartment building that you lease out forces you to save money every month via your mortgage payment.

Because some of that payment is going towards principal, you will be building equity and will be able to sell your home and get more cash out of it than you put into it (except for those unlucky souls who bought a house in 2006 and sold it in 2009).

Big crashes in the housing market are actually quite rare so we are going to set that scenario aside. Real estate is cyclical but it is generally not volatile. Besides, risk is the price you pay for returns. If there were zero risk, you’d get almost no return, like your savings account at the local bank.

It’s not all about single family homes you live in either. You can invest in office spaces, apartments, malls, and warehouses. Thanks to the catalyst in e-commerce same-day shipping that COVID provided, warehouses and stores now need to be closer to residential areas than they were before.

But there is very limited land and zoning available for warehouses in those areas. This naturally increases the demand for that space if it is located near the “last mile” or “last touch”. So commercial real estate is also a good option to diversify your money. My next post will discuss how I invest in commercial real estate without any complicated secrets.

Why Does Real Estate Go Up in Value?

You might know intuitively that real estate goes up in value (or you might know because the zestimates in your neighborhood are ludicrous). But do you know all the real reasons prices keep going up?

I’ve written before about the trends that I believe are going to keep this train moving up and to the right for a long time. Here are the highlights:

- Low interest rates have increased the demand for homes.

- Refinances over the past 2 years have caused many homeowners to stay put for awhile.

- Millennials now represent the largest age group in the United States and they all want houses. Not to mention there is a collective 70 trillion dollars in wealth transfer coming down the pike from Baby Boomers and the Silent Generation to their kids and grand kids.

- Remote work thanks to COVID permanently shifted many knowledge workers to full or part-time remote and so there is a premium placed on bigger and better living spaces since we spend more time in them.

- Credit scores are still very high for average homebuyers meaning there is far less risk in the housing market than there was in 2006 when strippers were buying their 3rd mansion in Miami with a credit score of 580 and 2% down.

- Thanks to stimulus checks, the child tax credits, and a record low number of vacations in 2020, many Americans are still flush with cash.

- The quality of new houses is vastly superior now than even just a few decades ago thanks to technology and standard of living changes.

- Builders are still reluctant to go crazy building new homes not to mention the skilled tradesmen for construction jobs are in high demand and short supply.

- Inflation. Real estate is an inflation hedge because while the purchasing power of the dollar is less and less each year (see the bullet point above and other such macroeconomic factors), your house payment remains fixed. So although the price of everything around you is increasing year over year, you are still spending the same amount on your monthly mortgage payment as you were the day you signed your loan.

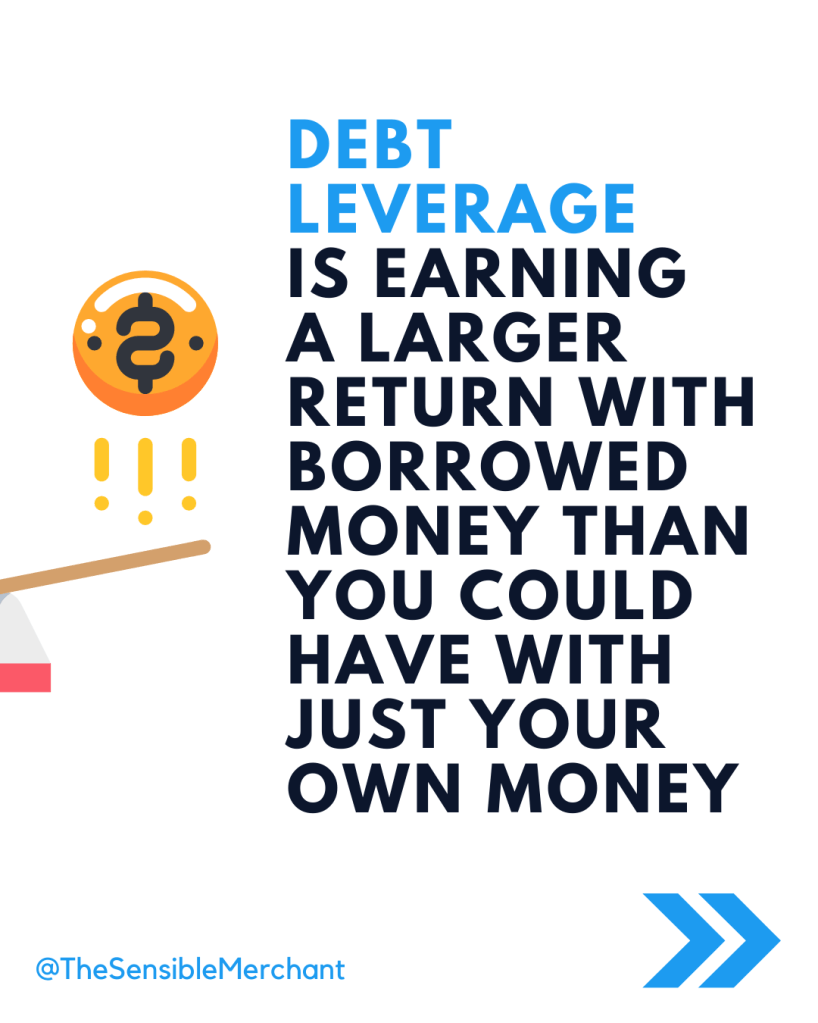

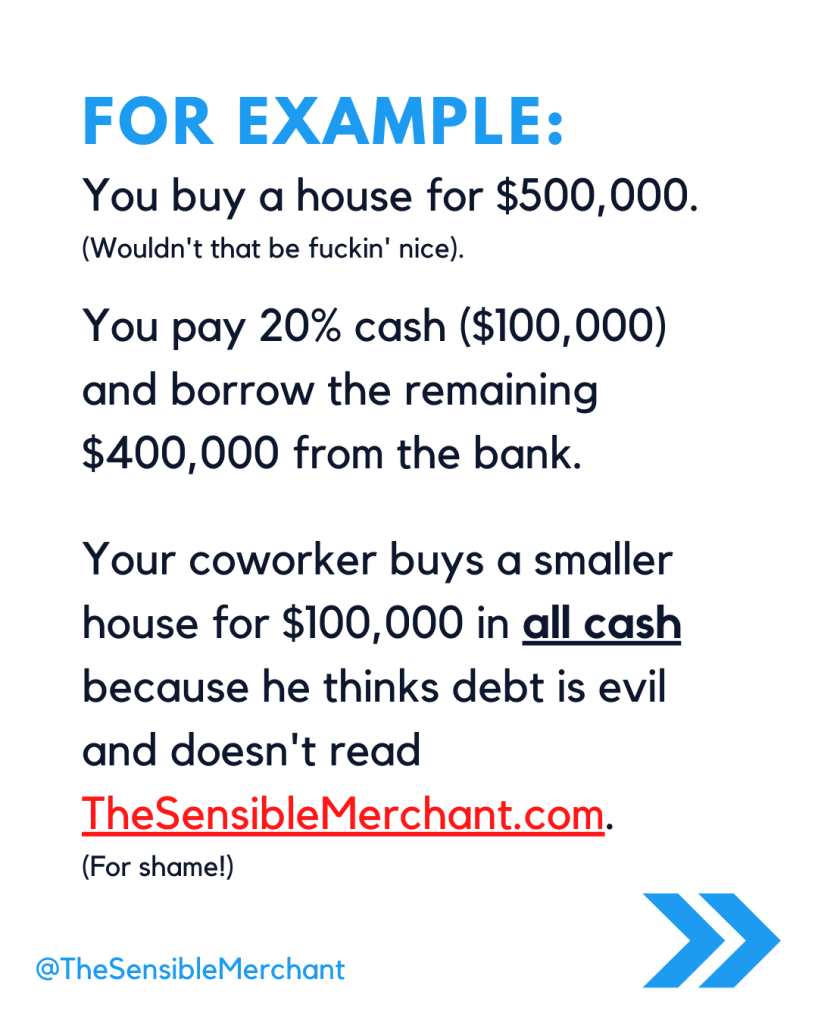

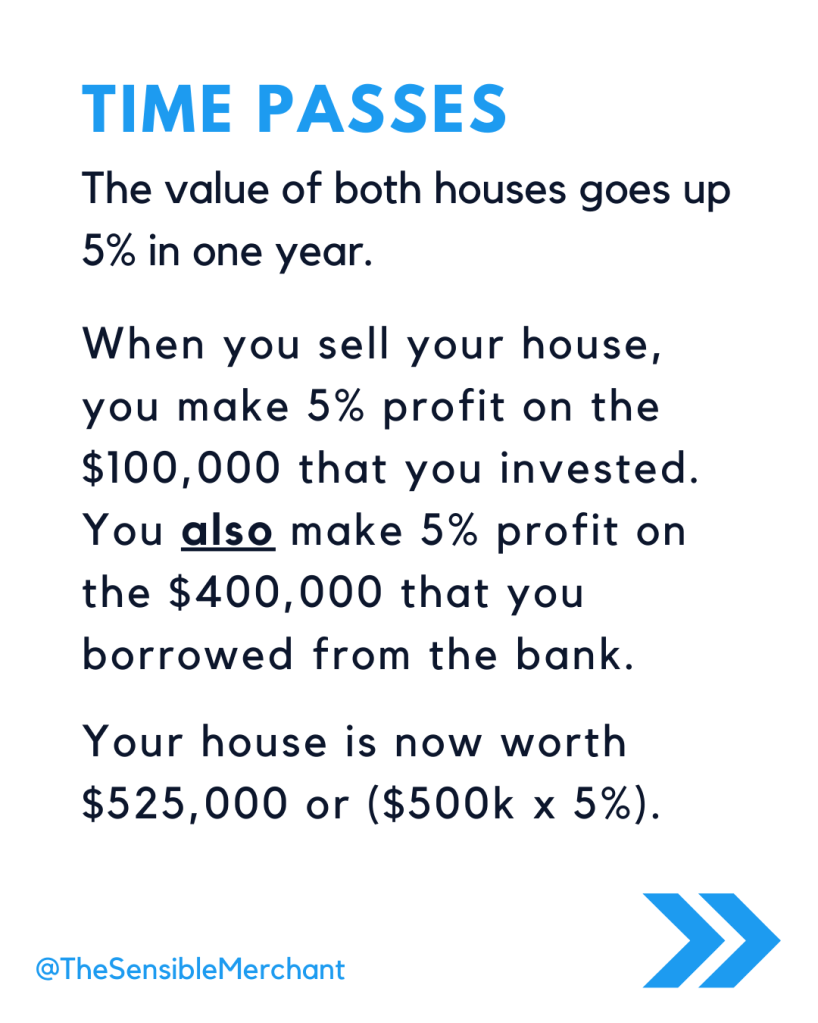

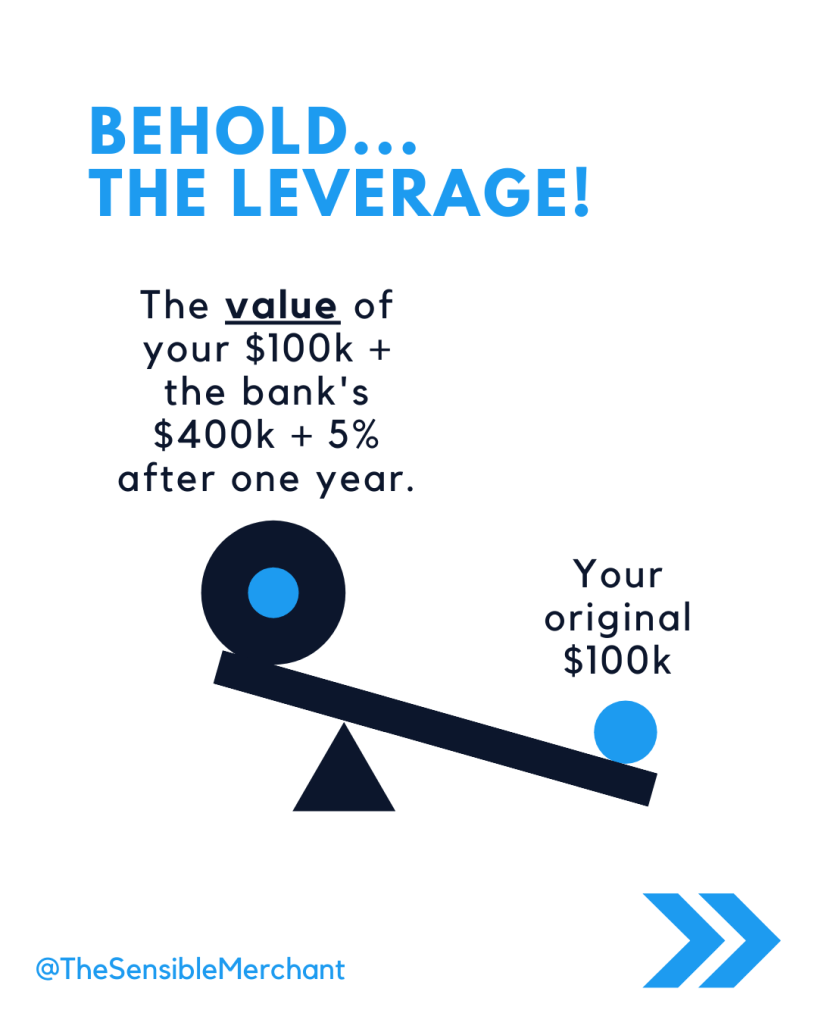

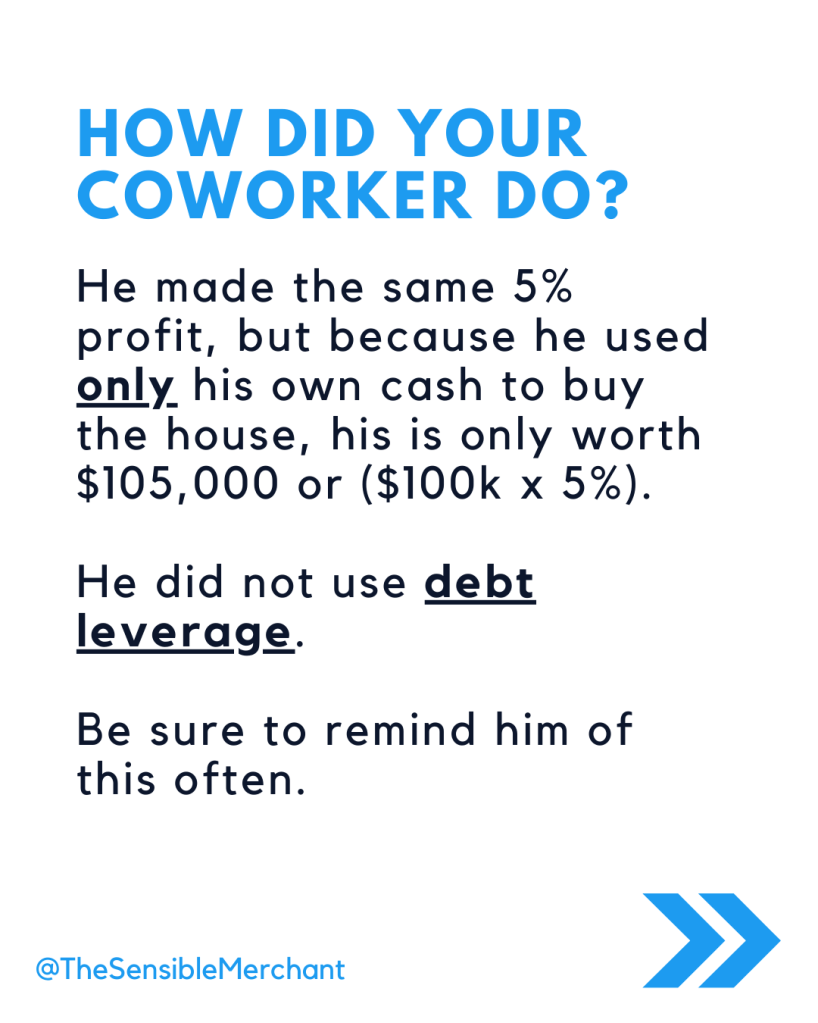

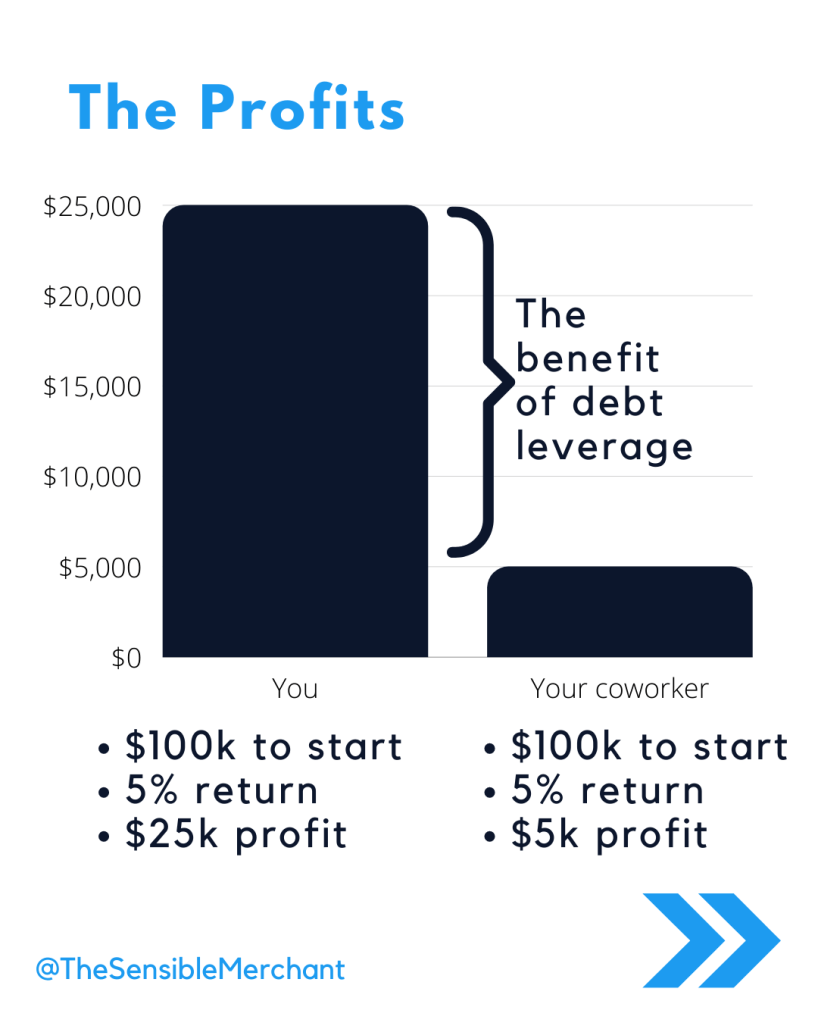

Debt Leverage

Lastly, I’ve created this fun little slideshow starring you and your idiot coworker to demonstrate the power of debt leverage when applied to purchasing your own house, an office space you will lease out, or an entire apartment community:

Having trouble coming up with the down payment for a house?

Check out my easy tips to save more money:

Here.

Here.

And here.

My next post is all about how I invest in real estate. Spoiler alert: it’s easier than you think.

Sign up for my newsletter to be notified of new posts (I won’t spam you. Promise.):

Related: Should You Build a New House or Buy Used?

More reading:

What Is a Buyer-Agent Agreement – And Why It’s the Smartest Move You Can Make When Buying a Home

Buying a home is too big of a decision to go it alone or leave it to chance. That’s where a Buyer-Agent Agreement comes in.

Keeping Up with Yourself

Keeping up with yourself can be a great fuel—and an even greater trap. The art is knowing when to press forward, and when to simply be where you are.

(5 min read)

Why You (and I) Need a Career Coach

I messed up at work but survived — thanks to my career coach. Spoiler alert: British football analogies included.

You must be logged in to post a comment.