In the 1960s, Allied Crude Vegetable Oil Company was engineering a corporate scandal that makes mismanaging risk at a regional bank seem quaint. And no, the scandal wasn’t their horrendously boring company name. Ba-dum-tss!

Allied Crude had been taking out big loans of cash in exchange for posting their oil inventories as collateral (similar to a mortgage or home equity line of credit wherein a homeowner takes out a loan and puts their house up as collateral in case they default on the loan and the bank could take the house).

The company would then take these loans to purchase soybean oil futures contracts, which would raise the price of the oil commodities on the market, thereby inflating the value of the oil the company held in inventories across the world.

This cycle fed on itself, making the owners and investors of Allied Crude wealthier and wealthier, and the banks giving them loans more and more susceptible to a hidden fraud with every passing day.

But nothing I’ve described so far is illegal. The crime only came to light when someone tipped off the authorities that about 90% of the company’s supposed oil inventory was actually water.

As you’ll recall from 7th grade science class, oil sits on top of water because it is less dense than water. Oil molecules are composed of hydrocarbons, which are lighter than water molecules and, therefore, float on the surface. Warehouses and ships filled to the brim with tanks of water and a little bit of oil on top of each. Inspectors couldn’t tell the difference.

But once the whistle had been blown, the bank found out, and oil prices plummeted. Those reputable banks which had given Allied Crude their loans, such as American Express, saw their stock prices cut in half upon the news.

Scandals, frauds, irresponsible risk-taking and volatility in the markets is as old as the markets themselves. That’s because markets are made up of humans and humans are motivated by incentives both good and bad and tend to take things too far.

The owner of Allied Crude Vegetable Oil Company had an incentive to lie about his oil inventories to make ungodly amounts of money in the oil futures markets. And the banks had an incentive to not look too closely at the tanks of “oil” because they were making good money on the loans they gave him.

Many people’s private finances may also be more water than oil if only they could be audited by outside observers.

We all know someone driving around in a brand new SUV with a brand new iPhone while living at home with their parents.

Or the person constantly posting pictures of their latest vacation while secretly confiding to you that they have no retirement savings. (Don’t forget, you can always take one trip now, or two trips later. Just depends what you value.)

Or the neighbor with the speed boat, snowmobile, second house up north and a $4,000 grill on their patio (you know it’s $4,000 because they tell you constantly).

Big flashy purchases like sports cars and exotic vacations are usually (but not always) a little bit of oil sitting on top of a bunch of water. And incentives play a role in these personal finance decisions.

People are often motivated to buy nice things to show others how successful they are. They can be incentivized by social media clout to post expensive vacation photos to show how worldly they are. They get satisfaction from having the most expensive car or the biggest house in the neighborhood. But at what cost?

Look no further than an account on every app called “Influencers in the wild” that showcases the oil/water dynamic perfectly. What you see on TikTok or Snapchat is the oil. But what’s really happening behind-the-scenes is all water:

Our old neighbors across the street were another example of this. They had a brand new Dodge Charger, a brand new F150, and a brand new house with a perfectly green lawn.

Then we noticed they stopped watering their grass. And soon we stopped hearing the roar of the Charger pulling into the driveway. Then a “For Sale” sign went up in the front yard.

When we stopped to talk to them one evening, they candidly told us they completely underestimated how much they were spending every month. They had an unplanned pregnancy and had to sell everything to be able to afford the baby.

I give them a lot of credit for being self-aware enough to change course and rebuild their lives somewhere else with a lower cost of living.

I’ve felt the water/oil dynamic at play in my own life, too. How often I would frame a shot for Instagram so that it looked more extravagant than it really was. How often I would daydream about driving a brand new BMW which, in reality, would only impress strangers I’d never meet while putting a strain on my finances and putting chains on my future economic freedom.

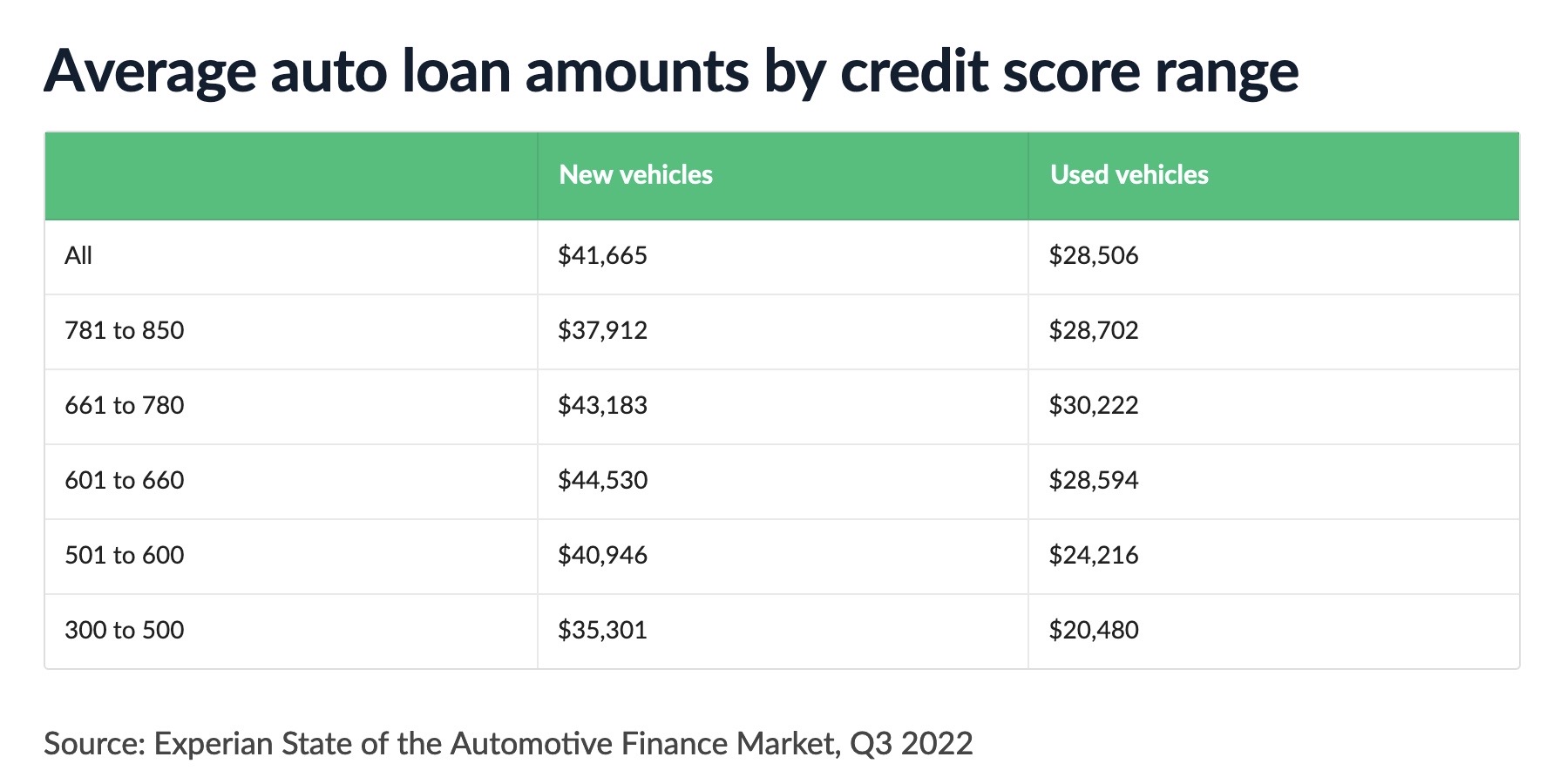

Many people may be making similar mistakes as evidenced by the car loan market these days:

Here we see that the highest loans on new vehicles are being taken out by people with a credit score of 601-660. That’s not a bad credit score, per se, but it’s certainly not great as it may signify low down payments, late payments, or a propensity to finance one’s life with debt.

In fact, the second lowest loan amount for new vehicles on the chart is being taken by people with the best credit scores.

I’ll caveat this by saying just because you have a low credit score does not mean you are financially irresponsible, but in the aggregate, it may portend a looming issue. As always, if you have a low credit score, follow these 5 simple tips to improve it.

Sam Bankman-Fried and FTX is another obvious example of this mirage at play. FTX was all water and no oil. In a world of zero percent interest rates, his sins were ignored. But the minute the FED took their foot off the gas and increased the cost of capital, the crimes came to light.

My takeaway from this is try not to put too much stock into what other people are doing with their money or life. Not being on social media helps lower the noise. And remember, you never know the full story. This is why I always try to stay skeptical of personal finance gurus.

And on the personal side, Morgan Housel said it brilliantly in a recent podcast, “Maybe the key to happiness with money is not figuring out how to get more, it’s figuring out how to want less”.

By spending some time thinking about what you truly value in life and then tracking your finances to ensure your spending is in line with those values, you won’t be tempted to cover up a bunch of water with a little bit of oil.

Subscribe here to be notified of each monthly article from http://www.poorchoices.org:

What Is a Buyer-Agent Agreement – And Why It’s the Smartest Move You Can Make When Buying a Home

Buying a home is too big of a decision to go it alone or leave it to chance. That’s where a Buyer-Agent Agreement comes in.

Keeping Up with Yourself

Keeping up with yourself can be a great fuel—and an even greater trap. The art is knowing when to press forward, and when to simply be where you are.

(5 min read)

Why You (and I) Need a Career Coach

I messed up at work but survived — thanks to my career coach. Spoiler alert: British football analogies included.

You must be logged in to post a comment.