Are we in a housing bubble in the United States?

Recency bias might lead us to believe we are. 2007 is still a fresh scar on the minds of many adults.

However, spoiler alert, I don’t think we are.

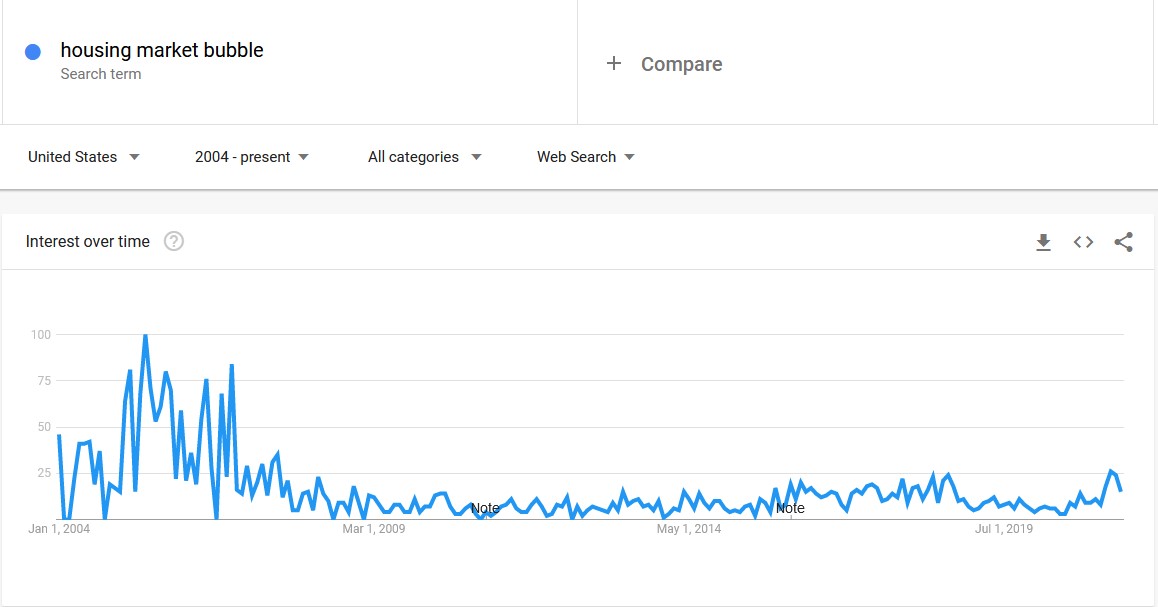

Google Trends seems to validate my opinion. Here’s a graph of the number of people searching for the term “housing market bubble” in the United States:

Not to say other markets aren’t. Bubbles seem to be popping all over the place recently. Whether you look at meme stocks, big tech, crypto currencies like Bitcoin and Ethereum, or SPACs, there are certainly areas that were or are still in a speculative bubble .

But so far, although housing prices remain red hot, I don’t think we can call them a bubble.

Allow me to define what I mean by bubble so we can all be on the same page.

Of course housing prices have risen quickly and are now out of reach for many first-time home buyers, but to call it a bubble would be to call it unsustainable, irrational, and driven by euphoria or greed more than pragmatism.

Today’s environment is unhealthy and will cool off in time, but for the moment, here’s why I don’t think the U.S. housing market is in a bubble:

Low Mortgage Interest Rates

When the Federal Reserve lowered interest rates at the onset of the pandemic, it gave a lifeline to many businesses and individuals who needed to borrow money to stay afloat. This is one of the levers the Fed can pull during economic calamities to get the economy moving again.

With low interest rates being set by the government and then passed along by mortgage lenders, new homeowners could borrow money for next to nothing. A lower interest rate means a lower monthly payment.

Housing prices are all about supply and demand.

This had the effect of increasing demand for homes so prices would naturally rise in this environment.

Refinances

With interest rates so low, many borrowers opted to refinance their mortgage instead of move during the pandemic.

When you refinance your mortgage, you pay a fee for the swap to payoff the original loan with the higher interest rate and secure a new loan at a lower interest rate. This fee can be bundled into the new mortgage and paid over the life of the new loan, or paid up front.

Either way, if you factor in the cost of that refinance, it wouldn’t make sense to sell your house right after doing that as the benefits of the refinance would be lost and there would be no point in paying the fees.

This is a supply limiting factor so with less supply of available homes on the market comes higher prices for those homes.

Millennials

Millennials were long disparaged as being lazy, stinky, ungrateful ne’er-do-wells more interested in their social media profile than a hard day’s work (at least according to the generation of boomers that raised them).

However, they now represent the largest age group of the United States population.

According to Pew Research, “With immigration adding more numbers to this group than any other, the Millennial population is projected to peak in 2033, at 74.9 million.”

This means that Millennials will continue to grow in size for another 12 years.

As they are entering their peak earning years and having babies, they’ll need houses. Some may opt to raise a family in an apartment, or be forced to, but many will simply suck it up and pay for high-priced houses.

This is a demand increasing factor and should be a tailwind for rising home prices.

Remote Work

Companies were forced to adopt remote schedules in 2020, and will be forced to have hybrid remote policies going forward to remain competitive.

Especially for couples or small families, working and living from home in an apartment or small house may not be feasible and they will require more square footage.

I believe this is a demand increasing factor and has permanently increased the value of homes.

One counter point is that homes can now be much more geographically dispersed than they were previously as folks won’t need to commute as often (or at all). This may have some effect on the regional dynamics of housing prices, but overall this seems like a bull case for housing prices right now.

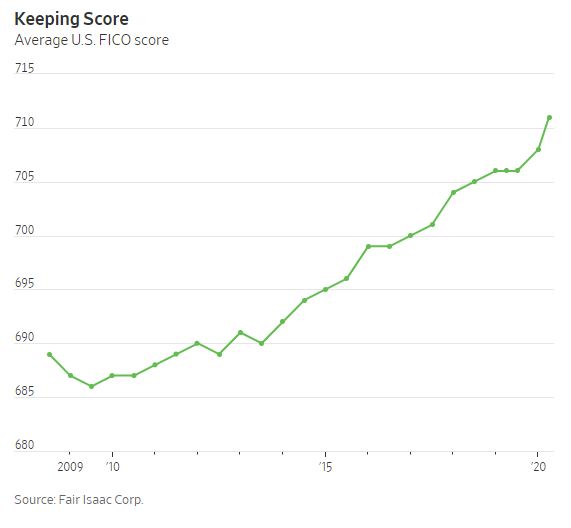

Credit Scores

Ever since credit scores took a dive due to foreclosures and bankruptcies during the Global Financial Crisis, they have been on a steady upward trend:

Higher credit scores indicate more responsible and capable borrowers that pay their bills on time, don’t overextend themselves with debt, and have long credit history.

According to The Motley Fool, “The median credit score among mortgage borrowers has increased steadily. And it hit a new record high of 786 in the fourth quarter of 2020. This is considerably higher than the overall average credit score in the U.S., which The Ascent’s research put at 706 in 2019.”

This means we are unlikely to witness a wave of foreclosures again like we did in 2007 and 2008, when lending requirements were far looser.

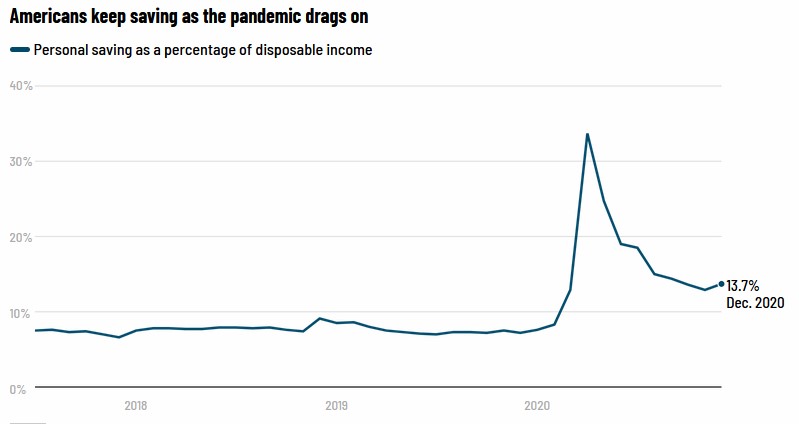

Savings Rates

Consumer spending plummeted in 2020 with nowhere to go and many folks now have record-high savings thanks to stimulus checks and permanent wage increases for lower income earners.

This is a demand increasing factor as more people have more cash than ever and are ready to spend it.

Inflation

Housing is an inflation hedge. As the government prints more money, each dollar becomes worth less and less. When that happens, the cost of goods rises, and so your home rises in value too.

And the government has been printing A LOT of money lately. Literally handing it out!

Inflation has historically been about 2-3% per year for the past 100 years. In his article, “Why Housing is a Good Hedge Against Inflation“, Ben Carlson explains how this helps mortgage borrowers:

The monthly payment on a $300k mortgage with a 3% fixed rate for 30 years is $1,265. That $1,265 includes both principal and interest payments (but not taxes).

After 10 years of 2% inflation, your monthly payment would now be 17% less at around $1,054. After 20 years, the inflation-adjusted monthly payment would be 32% less at $862. And your final payments in the last year of the loan would be 45% less than the original value or just $690 a month.

This is the beauty of inflation for people who own debt.

Quality of Houses

Yes, houses are expensive. But they are also way nicer than they used to be.

Growing up I never had air conditioning, double sink vanities off the master bedroom, or upstairs laundry. We didn’t have granite countertops, recessed lighting, or backsplashes in the kitchen. Our garage wasn’t big, our driveway wasn’t paved, and our floors weren’t hardwood.

This was true for most of my friends houses I visited too.

Nowadays, these luxuries are considered necessities for young couples buying their first house. The starter home is becoming a relic of the past.

Houses are bigger, nicer, and have more amenities than ever before. It makes sense that prices would rise as demand for updated houses increases.

Relatedly, homebuilders are building less starter homes than ever, because there isn’t as much profit in them.

This is both a supply limiting factor and a demand increasing factor.

The Takeaway

We have no idea where the housing market will go in the coming years. But I believe that all of these factors indicate it is at least sustainable.

Overall I believe these macro trends are more important than any anecdotes about bidding wars and geographic hot spots like Charlotte and Austin.

That said, buy for the long-term lifestyle, not the investment. Don’t take on a bigger payment than you can afford, don’t worry too much about what other people are doing, and don’t doomscroll on Zillow every night.

Sign up for my newsletter here:

More reading:

7 Lessons in Personal Finance from The Weasley Family of Harry Potter

7 evergreen lessons on personal finance from one of the most important wizarding families to ever live.

15 Questions to Ask When Buying a New Construction House

Consider the answers to these questions when deciding on a new home builder or a new construction house. (4 min read)

How to Scroll Responsibly (The Antidote to Social Media’s Negative Side Effects)

How we relate to social media can work for us or against us. These tips will ensure you keep a healthy perspective on your digital life. (4 min read)

10 Things to Consider When Comparing Apartments (Template Included)

Here are 10 things to consider when looking for a new apartment. (Free template included!)

You must be logged in to post a comment.