Listen to this blog post as a 5 minute podcast episode:

Stay Skeptical of Personal Finance Gurus – The Sensible Merchant

Rip Van Winkle

Rip Van Winkle is one of my favorite short stories. It’s absolute lunacy but has undeniable charm.

If you haven’t read it before, I recommend you do, but here’s a short summary:

Rip Van Winkle is always busy working on projects around town and at his neighbor’s farms but never does any work at his own farm. This is likely due to his nagging wife whom he dislikes and often hides from at the local tavern.

Well, his wife finds him there, too, so he leaves town and wanders into the Catskill mountains in the Appalachians. Here he finds some Dutch strangers who are having a real party up there. He steals a sip of their magical mead and falls asleep. He wakes up 20 years later with a long beard and a rusty gun next to him where his nice, polished one was before he fell asleep.

He wanders back down to town but no one recognizes him and the buildings are all different. He finds out from the local villagers that his wife died while yelling at a door-to-door salesman and his daughter has a son now at her own farm. He ends up moving in with her and living out the rest of his days, too old to do any real work.

The end.

What a legend.

Well Rip wasn’t the only one neglecting his duties while doing something as crazy as partying with the Dutch up in the mountains… while I was busy worrying about getting my retirement accounts ready for a revolution, I overlooked a simple fact: if I max out my 401(k) too early in the year, I won’t get the employer match for those non-existent contributions later in the year.

Apparently, I was too busy partying down at the tavern to keep an eye on my proverbial farm.

See, normally at the beginning of the year, I set my contributions to a high percentage of my paycheck, go without much income, and rely on my savings.

Personally, I like to front-load the account so that I’m not tempted to spend any extra money until the account is maxed out. Once I meet the $19,500, I’m far more likely to splurge and use the money for fun non-essentials because I know I’ve saved enough for the year.

Pay yourself first and you’ll never have to worry about a budget.

Then, once I near the limit (which is $19,500 as of 2021) I reduce it down to the minimum percent to still receive the maximum employer contribution.

This year, I forgot about it until I noticed the employer match was missing from my latest paystub. Just one paycheck at 80% contributions can tilt my whole system out of whack.

I’m kicking myself for not paying closer attention. This amounts to about $800 of missed employer matches going forward. I’m grateful to be in a position with my savings that I can even max it out to begin with, but that stings. It’s literally free money.

Lesson learned, pay attention to my own farm… I mean 401(k).

But then combine this with how amazing a portfolio could be if you diversified into low cost index funds, dollar-cost-averaged, and then fell asleep for 20 years? Rip Van Winkle would have woken up to some stellar returns.

If Rip had invested $19,500 into an S&P 500 index fund on September 20, 2001, and then annually made that same investment, his portfolio would be worth $1.5 million today. Zero effort required. No day trading, reading headlines, or fancy finance degree required either.

“Set it and forget it” is the ultimate technique to building wealth and one of the biggest advantages retail investors like you and I have over actively managed funds.

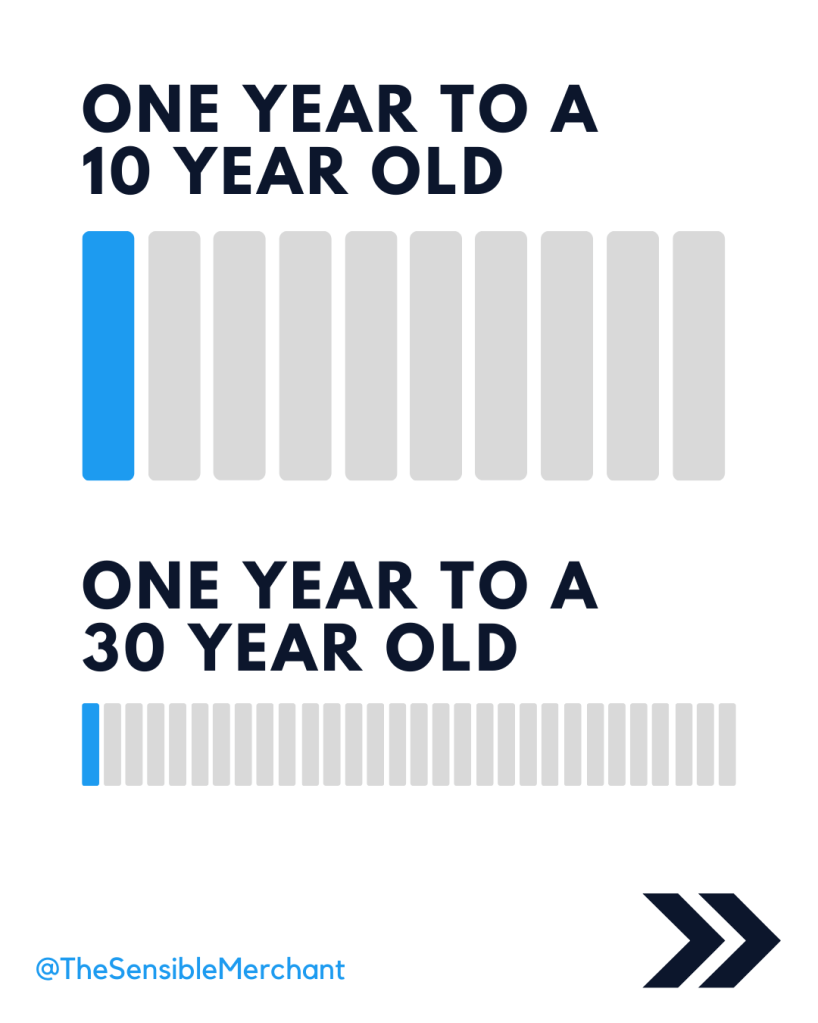

The final lesson from this story is just how quickly time seems to go, even when we’re awake!

Attempting to max out your 401(k) may not seem relevant at age 25, or 35, or even 45. But Rip fell asleep one night and woke up as if no time had passed at all, only to realize everything he knew was changed or gone altogether. That’s a lot how my life feels these days.

I will drive past areas of town I haven’t visited in a year or two and there’s entirely new buildings seemingly built out of thin air.

There’s this interesting phenomenon that the older we get, the less a single year means to us, so the less we remember it.

We put things off only to wake up one day and realize it feels too late to even start.

I created this to illustrate this fact @TheSensibleMerchant on Instagram:

Use this as a reminder to go check your balance and see if you need to increase/decrease your contributions for the rest of the year. Thankfully, the difference between us and our friend Rip is that we can wake up at any moment and correct course… if only we are paying attention.

Here’s some other thoughts on 401(k)s:

Why Front-load a 401(k)?

Assuming you don’t have the risk that you’ll fall asleep for 20 years in the Catskills, there are actually a couple different reasons why someone might want to front-load their work sponsored retirement account.

For one, if we are in a bull market, front-loading the account means you will realize more gains. This is like trying to time the market, though, and likely won’t work every year. It could even backfire if the market is at an all-time high early in the year and then has a crash later in the year. You could also have the opposite risk if you back-load it.

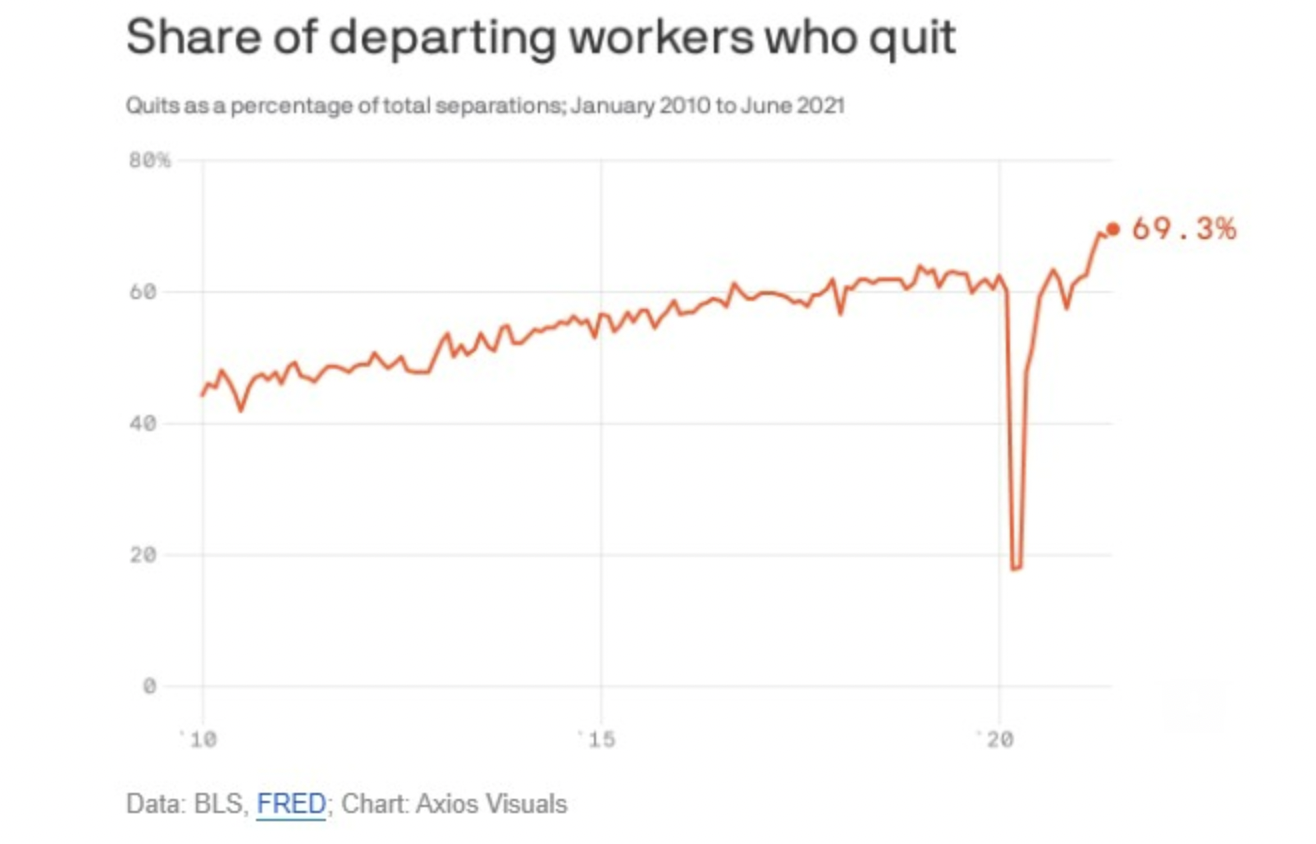

Another reason is if you plan to retire, quit your job or otherwise take time away from work where you won’t be getting income later in the year. In today’s world of high quit rates, this could be more common. Just look at how many people are voluntarily leaving jobs this year:

Some of these people may be going on to start their own businesses where they won’t have access to a company sponsored retirement plan so they will want to bank as much as possible before leaving.

How to Max Out Your 401(k) in Equal Increments

If you want a “set it and forget it” method to max out your 401(k) in equal increments, just take the maximum (which, again, is $19,500 this year) and divide it by 27 (the number of pay periods in a year assuming you get paychecks every other week). This comes out to $720.

Tweak the percentage of your contributions to land at this dollar value each check. This should get you to a place where you can dollar cost average throughout the year and won’t have to miss out on any employer matches like me.

If you do make the same mistake as me, some companies offer “true-ups” to reimburse you on missed contributions for this exact reason. Unfortunately, like Rip Van Winkle’s wife, my company apparently hates me and does not offer them.

For more fairy tales with shoe-horned personal finance lessons, subscribe to my newsletter:

More reading:

7 Lessons in Personal Finance from The Weasley Family of Harry Potter

7 evergreen lessons on personal finance from one of the most important wizarding families to ever live.

Keep reading

Build a Fortress Out of Your Money

Use the strongest castle in Europe as a blueprint to draft the best defense for your money. (4 min read)

Keep reading

Stay Skeptical of Personal Finance Gurus

When personal finance advice goes from “helpful” to “smoke and mirrors” and finally to “harmful”. (5 min read)

Keep readingMy latest Instagram posts:

You must be logged in to post a comment.